CBO’s 2024 Long-Term Projections for Social Security

August 28, 2024 - Congressional Budget Office

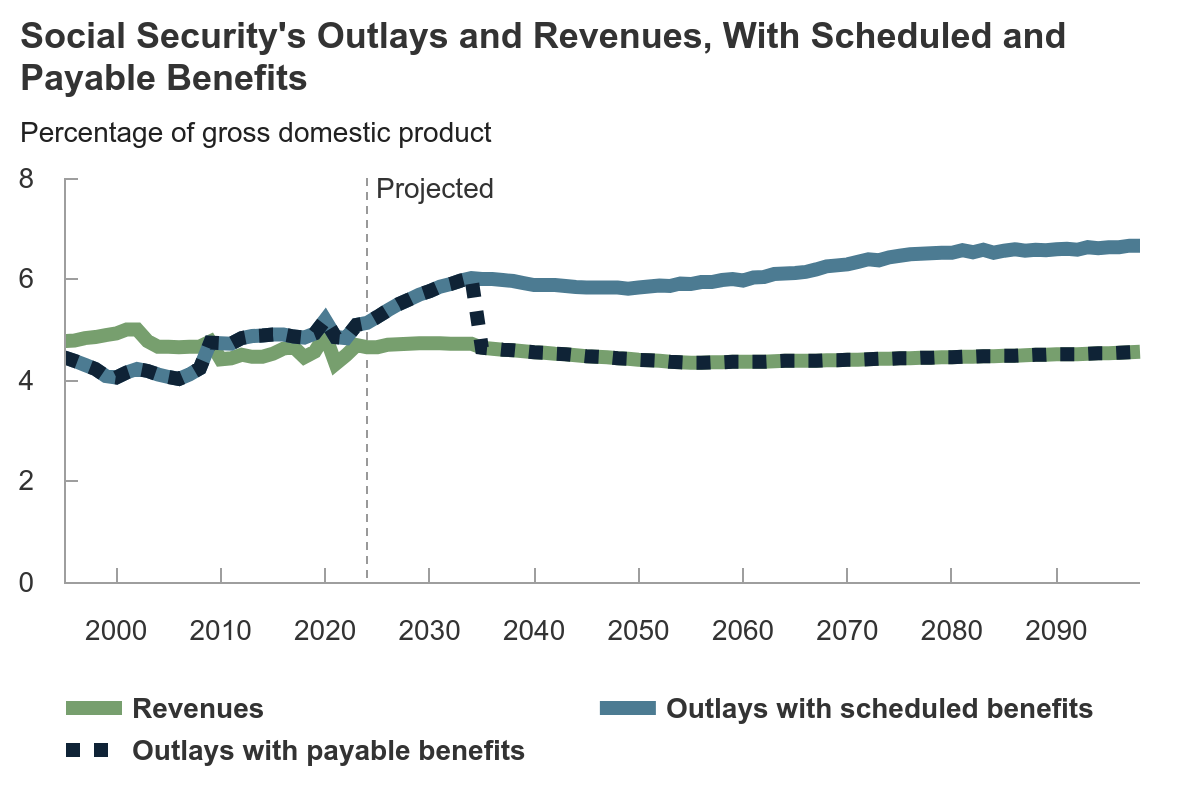

In CBO’s projections, spending for Social Security rises relative to GDP over the next 75 years, and the gap between outlays and revenues widens. If combined, the balances in the program’s trust funds would be exhausted in fiscal year 2034.

In this report, the Congressional Budget Office describes its 75-year projections for the Social Security program. One set of projections reflects a scenario in which the program continues to pay retirement, disability, and related benefits as scheduled under current law, regardless of whether the program’s two trust funds have sufficient balances to cover those payments. The second set of projections reflects a scenario in which Social Security’s outlays are limited to the amounts that can be paid from the program’s annual revenues after the combined balance of the trust funds is exhausted『hich is now projected to occur in fiscal year 2034.

- Social Security’s Finances, With Scheduled Benefits. CBO projects that if Social Security paid benefits as scheduled, spending on the program would increase from 5.1 percent of gross domestic product (GDP) in 2024 to 6.7 percent in 2098. That increase is attributable to the growing share of the population age 65 or older. The program’s revenues would remain near 4.5 percent of GDP during that 75-year period. After 2098, the gap between revenues and outlays as a percentage of GDP would widen, and shortfalls would continue to grow.

In CBO’s projections, the balance of the Old-Age and Survivors Insurance Trust Fund is exhausted in fiscal year 2033, and the balance of the Disability Insurance Trust Fund is exhausted in 2064. Social Security’s actuarial deficit over the next 75 years, a summary measure of the program’s sustainability, is equal to 1.5 percent of GDP or 4.3 percent of taxable payroll (total earnings subject to the Social Security payroll tax). - Distribution of Scheduled Benefits and Payroll Taxes. Average initial benefits are projected to increase over time in real terms (that is, after adjustments to remove the effects of inflation). For people born from the 1950s to the 1990s, those initial benefits replace more than one-third of preretirement earnings for retired workers and more than half of average recent earnings for disabled workers. Within a cohort of Social Security recipients who were born in the same decade, people with higher earnings generally receive larger benefits than people with lower earnings, but those larger benefits replace a smaller share of their previous earnings. People with higher earnings also generally pay a larger dollar amount|ut a smaller share of their lifetime earnings(n Social Security payroll taxes. The Social Security program is progressive in that lifetime benefits tend to be larger relative to lifetime payroll taxes for people with lower earnings than for people with higher earnings.

- Social Security’s Finances, With Payable Benefits. If Social Security’s outlays were limited to the amounts that could be paid from annual revenues after the combined balance of the trust funds was exhausted in fiscal year 2034, benefits would be about 23 percent smaller than scheduled benefits in 2035, CBO projects. Payable benefits would be about 28 percent smaller than scheduled benefits in 2098.

- Distribution of Payable Benefits. In the payable-benefits scenario, average initial retirement benefits resume growing over time after the combined balance of the trust funds is exhausted. But those benefits are smaller than scheduled benefits for people born after 1969 (who turn 65 after 2034).